The numbers have moved past debate. In 2026, the question is no longer whether AI will reshape technology and work — it is whether your organisation is positioned to benefit from the transformation already under way.

Every few decades, a technology arrives that does not merely improve an existing process but changes the frame entirely. The printing press, the steam engine, electrification, and the internet all shared a common trait: they looked, at first, like tools, and only later revealed themselves to be infrastructure. Artificial intelligence is doing the same thing right now, and the pace of the shift is compressing what previous revolutions measured in generations into something closer to a handful of years.

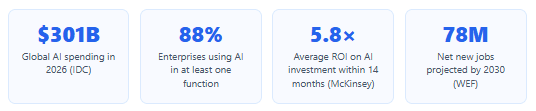

By mid-2026, global AI spending has reached $301 billion — up from $223 billion in 2025 — and 88% of enterprises report using AI in at least one business function. These are not pilot figures. They are production numbers from organisations that have moved past experimentation and are now treating AI as operational infrastructure. What follows is an honest account of where that infrastructure stands, what it is delivering, where it still struggles, and what it means for the people who build and work with software for a living.

The Scale of What Is Already Happening

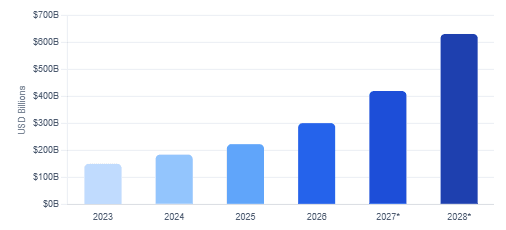

It is easy to read technology trend articles and conclude that the numbers are aspirational — projections dressed up as facts. The 2026 figures, however, are largely backward-looking measurements of things that have already occurred. The AI market stood at $390.9 billion in 2025 and is growing at a 30.6% compound annual rate toward a projected $3.5 trillion by 2033. ChatGPT crossed 900 million weekly active users by March 2026. GitHub Copilot reached 20 million users and is now deployed at 90% of Fortune 500 companies. These are not headline-grabbing forecasts — they are current usage statistics.

Underneath the consumer-visible layer, the enterprise picture is more nuanced but equally significant. 72% of large enterprises have adopted some form of AI automation, and businesses that have done so report an average 35% reduction in operational costs within the first year. Furthermore, organisations using AI in IT operations report 31% fewer critical incidents and 28% faster mean time to resolution. For engineering teams, that last statistic is particularly meaningful — it represents AI doing what monitoring dashboards and runbooks alone never quite managed to do.

That said, the transition is uneven. As of early 2026, only 8.6% of companies have AI agents deployed in production, while 63.7% report no formalised agent strategy at all. The gap between AI adoption in general and AI agents in production reflects a genuine complexity jump — going from a language model that helps a developer write a function to an autonomous agent that orchestrates multi-step workflows across systems is a fundamentally different engineering challenge.

Global AI Spending — 2023 to 2028 Forecast (USD Billions)

How Different Industries Are Being Reshaped

AI adoption does not look the same across sectors. Each industry is being reshaped according to where its data concentrations, regulatory constraints, and labour cost structures sit. Understanding those differences matters, because the lessons from one sector often preview what is coming in another.

Software Development

For the audience reading this publication, software development is the most immediately relevant domain. The evidence here is consistent and significant. AI-assisted developers produce 40–55% more code per week, according to GitHub’s own research, though code quality metrics vary considerably by implementation. More meaningfully for organisations, AI tooling is compressing the gap between junior and senior developers — not by replacing experienced engineers, but by accelerating the output of less experienced ones and reducing the volume of routine, low-cognition work that previously consumed a disproportionate share of senior engineers’ time.

The Stanford HAI 2026 AI Index found that AI-related skills now appear in 2.5% of all US job postings — a 297% increase over the past decade, growing roughly twenty times faster than the overall job market. Meanwhile, workers with advanced AI skills earn 56% more than peers in the same roles without them, according to PwC. The implication for engineers is direct: AI fluency is now a compensation differentiator, not merely a resume item.

Healthcare

Healthcare AI is moving from experimental to clinical at a pace that would have seemed implausible five years ago. AI diagnostic tools now assist radiologists, pathologists, and cardiologists in identifying patterns that human review alone would miss or delay. Predictive models flag deteriorating patients hours before standard vital-sign thresholds would trigger an alert. Administrative AI is handling scheduling, prior authorisation, and clinical documentation — arguably the single largest source of physician burnout in the current system. The WEF describes healthcare as seeing explosive growth in AI-assisted roles precisely because the domain combines vast structured data, repetitive cognitive tasks, and high-stakes decisions — a profile where AI augmentation delivers consistent value.

Manufacturing and Supply Chain

Manufacturing was the first industry to feel the impact of narrow automation, and it is now the first to be feeling the second wave. AI-powered process automation and quality control have delivered an average 23% reduction in downtime for manufacturers who have deployed them. Predictive maintenance, the application of machine learning to sensor data to forecast equipment failures before they occur, is reducing both downtime and maintenance costs in ways that traditional scheduled maintenance never achieved. Supply chain AI is doing something more structurally significant: it is absorbing the complexity of real-time disruption prediction across global supplier networks that human planners simply cannot monitor at the required scale.

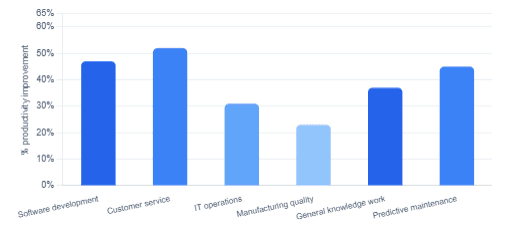

AI Productivity Impact by Business Function — Average Improvement (%)

The Workforce Question: Displacement, Creation, and the Net

No honest discussion of the AI revolution can avoid the workforce question, and no honest answer to that question is simple. The data points in multiple directions simultaneously, and that ambiguity is itself informative.

The most widely cited projection comes from the World Economic Forum’s Future of Jobs Report, which projects that between 2025 and 2030, 170 million new jobs will be created while 92 million are displaced — a net gain of 78 million positions. Gartner, separately, projects that AI will create more jobs than it destroys by 2028. These headline numbers are often reported without their important caveat: the new jobs and the displaced jobs do not go to the same people, in the same geographies, or on the same timeline. That mismatch is where the genuine human cost of the transition lives.

Sectors like manufacturing, customer service, and transportation face significant near-term disruption, while technology, healthcare, and education are seeing growing demand. The EU AI Act, the world’s first comprehensive AI regulation, now classifies workplace AI uses such as recruitment and performance evaluation as high-risk, requiring transparency, human oversight, and worker notification. Meanwhile, the act’s provisions on emotion recognition in the workplace have been in force since February 2025. Regulation is, for once, following the technology at close distance rather than arriving years late.

The pilot purgatory problem: Despite high adoption rates, as of early 2026 nearly two-thirds of organisations remain stuck in the pilot stage — having not begun scaling AI across the enterprise. High adoption does not automatically translate to value. The organisations seeing the 5.8× ROI cited by McKinsey are those that moved from experiment to production and built the organisational muscle to run AI continuously, not just demonstrate it.

| Sector | Primary AI application | Near-term outlook | Key metric |

|---|---|---|---|

| Software development | Code generation, review, testing | Growing demand | 40–55% more code per week |

| Healthcare | Diagnostics, admin automation | Growing demand | Explosive role growth (WEF) |

| Manufacturing | Predictive maintenance, QA | Mixed — disruption + gain | 23% downtime reduction |

| Customer service | Tier-1 ticket resolution | Significant displacement | 68% Tier-1 resolved without humans |

| IT operations | Incident detection, remediation | Growing demand | 31% fewer critical incidents |

| Transportation / logistics | Route optimisation, autonomous systems | Near-term displacement risk | Supply chain disruption prediction |

Agentic AI: The Next Threshold

If the current phase of the AI revolution is characterised by tools that augment human work — copilots, assistants, recommenders — the next phase is defined by agents that operate autonomously across multi-step workflows. Agentic AI is not a distant prospect. Deloitte forecasts that 50% of organisations currently using generative AI will have launched agentic AI pilots by 2027. Gartner projects that by 2028, at least 15% of day-to-day business decisions will be made autonomously by agents — up from essentially zero in 2024.

For software engineers, this transition has concrete implications. Agentic systems require different engineering disciplines than traditional application development. Orchestration, reliability under partial failure, prompt engineering at scale, observability of autonomous reasoning chains, and the governance of AI decision-making in regulated contexts are all becoming core competencies. The Business Process Automation market is projected to reach $16.46 billion in 2025, growing at a 10.7% CAGR — a market that agentic AI is poised to expand and transform simultaneously.

The opportunity for engineers: Agentic AI is creating a new category of technical role that sits at the intersection of software architecture, ML systems, and product thinking. Early movers into this space — those building the orchestration layers, evaluation frameworks, and guardrail systems that make agents trustworthy — are working on infrastructure that will underpin the next decade of software development in much the same way that cloud-native tooling did the last one.

Responsibility, Regulation, and the Human Element

The speed of AI adoption has outpaced regulatory frameworks in most jurisdictions, though that gap is closing. The EU AI Act is the most comprehensive legislation to date, but it is also the product of a regulatory process that began before large language models existed in their current form. The result is a framework that is broadly sensible but imperfectly calibrated to the specific risk profiles of generative and agentic AI. The provisional agreement reached in May 2026 to overhaul key parts of the Act — pushing back enforcement deadlines while strengthening transparency requirements — reflects the genuine difficulty of governing a technology that is itself rapidly evolving.

Beyond legislation, there are deeper questions about how AI systems are built and deployed responsibly. Bias in training data propagates into production outputs. Opaque decision-making in high-stakes domains — credit, hiring, healthcare — raises legitimate concerns about accountability. The energy consumption of large model training and inference is a real environmental cost that the industry has been slow to address transparently. None of these are arguments against AI adoption; they are arguments for AI adoption done with genuine engineering discipline and ethical seriousness.

There is also something worth saying about the human element that AI, however capable, does not replace. The professionals who stand out in 2026 are those who combine AI tool fluency with contextual judgment, creative thinking, and interpersonal capability — qualities that remain distinctively human. The most compelling framing of the AI revolution is not replacement but augmentation: a developer who understands AI deeply is not at risk of being replaced by AI — they are at risk of being replaced by another developer who understands AI deeply. The distinction matters.

Embracing the Revolution Without Losing the Plot

Embracing the AI revolution does not mean adopting every tool the moment it ships, or betting organisational strategy on capabilities that are still maturing. It means developing a clear-eyed understanding of what AI does well today, what it will do well in three years, and how to build organisational muscle — technical, cultural, and operational — to absorb and benefit from the transition continuously.

For engineering organisations specifically, that means several concrete things. It means making AI literacy a first-class engineering competency, not a nice-to-have. It means building evaluation and observability infrastructure for AI systems with the same rigour applied to production services. It means establishing governance frameworks for AI decision-making before those decisions are consequential enough to attract external scrutiny. And it means treating the workforce transition honestly — investing in reskilling, communicating transparently about how roles will evolve, and recognising that the organisations most likely to navigate the transition well are those that treat their people as the primary asset being augmented, not the primary cost being reduced.

| Action | Why it matters now | Risk of waiting |

|---|---|---|

| Build AI literacy across engineering teams | Skill premium already at 56% salary differential | Talent gap compounds exponentially |

| Move pilots to production | 5.8× ROI only materialises in production | Competitors in pilot purgatory have same risk |

| Invest in AI observability | Agents require different monitoring than APIs | Silent failures with high blast radius |

| Engage with AI governance frameworks | EU AI Act enforcement already in motion | Retroactive compliance is always more costly |

| Plan workforce transition explicitly | Role changes are measurable and already occurring | Reactive restructuring is more expensive and more damaging |

What We Learned

The AI revolution is not a future scenario — it is a present-tense infrastructure shift. We covered the scale of what has already happened: $301 billion in global AI spending, 88% enterprise adoption, and productivity gains that are measured, not modelled. We examined how different industries are being reshaped at different speeds and in different ways, from the 40–55% productivity uplift in software development to the 23% downtime reduction in manufacturing and the near-term displacement pressures in customer service and transportation. We looked honestly at the workforce question, acknowledging both the WEF’s net positive projection of 78 million new jobs and the genuine human cost of the transition for workers whose skills map to the displaced side of that equation. We traced the emerging frontier of agentic AI and what it demands from engineering organisations. And we explored the regulatory and ethical landscape that is, finally, beginning to catch up with the technology. Throughout, the consistent finding is the same: the organisations and individuals who are thoughtfully embracing the AI revolution — not uncritically, not fearfully, but with genuine competence and clear-eyed strategy — are the ones best positioned to benefit from what comes next.