Telling engineers to “just refactor it” is a bit like telling a country to “just pay off its national debt.” The advice is technically correct, financially naive, and misses the entire point. Technical debt is not a failure of discipline — it is often the output of perfectly rational decision-making under real constraints.

1. The Debt Metaphor Is More Literal Than You Think

Ward Cunningham coined the technical debt metaphor in 1992 while developing a portfolio management system at WyCash — a fact that is pleasantly appropriate, given the financial context. He needed to explain to business stakeholders why the team had to budget time for refactoring. His metaphor: shipping first-time code is like borrowing money. You move faster now, but you pay interest until you repay the principal.

As Cunningham put it at the time, “shipping first time code is like going into debt. A little debt speeds development, so long as it is paid back promptly with a rewrite… The danger occurs when the debt is not repaid. Every minute spent on not-quite-right code counts as interest on that debt.” Crucially, Cunningham was not condemning the decision to take on debt. He was using a financial instrument as a model. And like financial instruments, debt is only irrational when the terms are bad — not by its existence.

Martin Fowler later extended this into the Technical Debt Quadrant, distinguishing between deliberate and inadvertent debt, and between prudent and reckless debt. The quadrant is useful precisely because it separates the moral judgement from the economic one. Prudent deliberate debt — shipping a known shortcut to hit a launch window — is categorically different from reckless inadvertent debt — writing bad code because the team did not know better. Yet in most engineering conversations, both are treated identically, and both receive the same response: “you should fix that.”

“Technical debt is like dark matter: you know it exists, you can infer its impact, but you can’t see or measure it.”— McKinsey Digital, “Tech debt: Reclaiming tech equity”

The McKinsey description is apt. But dark matter, of course, is not good or bad — it simply has mass and exerts gravity. The question is whether you account for that gravity correctly in your trajectory planning. Most teams do not. And the reason is not laziness. It is economics.

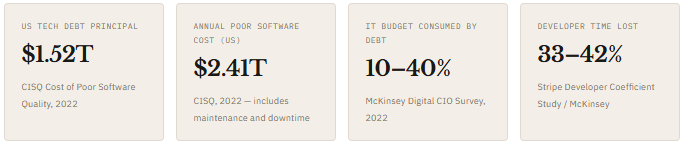

2. The Numbers Are Not Abstract

Before getting into the economic models, it is worth grounding the discussion in scale. Technical debt is not a niche concern or an academic problem. It is one of the largest line items in the global technology budget, and it is growing.

The McKinsey 2022 study, which examined 220 companies across five geographies and seven sectors, found a direct correlation between technical debt ratio and business performance. Companies in the 80th percentile for their Tech Debt Score had revenue growth that was 20 percent higher than those in the bottom 20th percentile. Furthermore, for more than 50% of companies, technical debt accounts for greater than a quarter of their total IT budget, blocking otherwise viable innovations if not addressed.

Those numbers describe the aggregate cost of debt that was poorly managed. They do not, however, describe whether taking on that debt was irrational at the time. To understand that, you need economic models — specifically, the concepts of discount rates, option value, and game theory payoff structures.

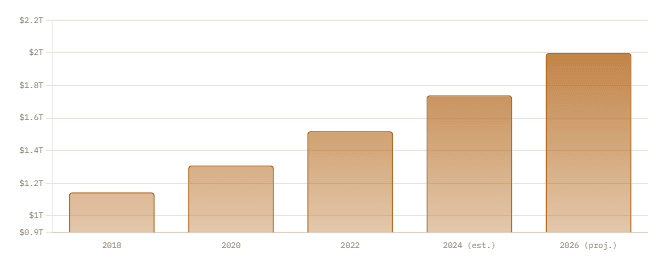

Technical Debt Principal Growth in US Software (CISQ Estimates)

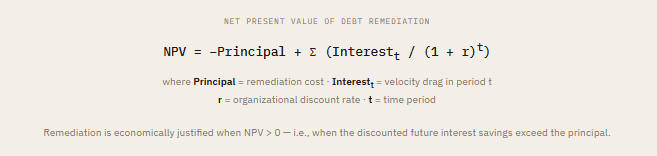

3. Discount Rates: Why Future Pain Feels Cheap Today

The core of rational debt accumulation is temporal discounting — the well-established economic and psychological principle that future costs and benefits are valued less than present ones. In financial modeling, this is expressed through a discount rate: a percentage that reduces the present value of a future cash flow for each year of delay. A dollar you owe in ten years, discounted at 10% per year, is worth about 38 cents today.

The same logic applies to technical debt. A refactoring cost that your team will pay in two years feels cheaper than a feature shipping delay that costs your company revenue today. The question is not whether that discounting happens — it always does. The question is whether the implicit discount rate being applied is appropriate.

For a stable enterprise with a 10-year runway, a discount rate of 8–12% is reasonable — it roughly matches the cost of capital. At that rate, debt that slows the team by 15% over three years has a clear positive NPV for remediation. But for a startup facing a Series A pitch in four months, the effective discount rate on anything beyond the next quarter can be 200% or more. At that rate, nearly all future interest is discounted to near zero — and taking on debt is genuinely the right call.

This is why the same technical shortcut can be the correct decision at a startup and the wrong decision at a mature enterprise. The code is identical. The economics are completely different. Intertemporal choices, where distant outcomes are often valued lower than short-range ones, lead to temporal discounting — a phenomenon which over and over leads to unmanageable technical debt. The research is careful, however, not to call this irrational. At high enough discount rates, discounting future costs heavily is the correct response to uncertainty about whether those future costs will ever be paid.

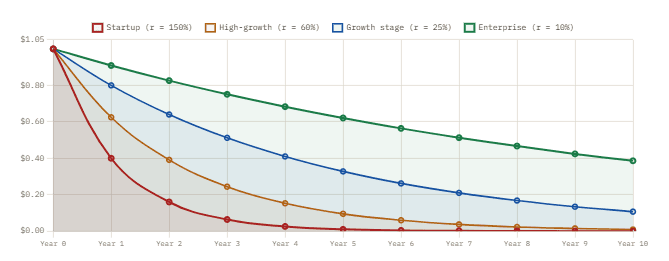

Present Value of $1 of Future Tech Debt Interest at Different Discount Rates

The practical implication is important: when engineering leadership argues for prioritizing debt remediation, they are implicitly arguing that the organization’s real discount rate is lower than the one being applied by product and business stakeholders. That is a legitimate economic disagreement, not a technical one. Framing it as a technical argument — “the code is messy” — is both less persuasive and less honest than framing it as a financial one: “we are discounting our future costs at a rate that does not match our actual time horizon.”

4. Option Value: The Case for Deferring

There is a second economic argument for accumulating technical debt that even most advocates of refactoring do not adequately address: option value. In financial economics, an option is the right — but not the obligation — to take a future action. Options have value precisely because the future is uncertain. Keeping your options open is worth paying for.

Technical debt, in certain contexts, functions as a way of preserving option value. Consider a team building a new product feature with uncertain product-market fit. Investing heavily in clean architecture, comprehensive tests, and well-factored abstractions makes sense if that feature will be the foundation for the next five years of development. But if there is a 60% chance the feature will be completely redesigned or discarded based on user feedback, that investment has negative expected value. The technically correct approach — measured against the actual decision landscape — is to ship a pragmatic implementation, learn from users, and only refactor if the feature proves its worth.

Real Options TheoryThe application of real options theory to software decisions — sometimes called “Software Real Options” — suggests that the flexibility to delay architectural investment until requirements are clearer has measurable positive value. The option to refactor later is worth more than zero. This means that even if immediate refactoring produces a “better” codebase, the decision to wait may still be economically superior when properly accounting for uncertainty.

This is not merely theoretical. The well-documented failure mode of over-engineering — building elaborate architectures for requirements that never materialize — is precisely what happens when teams ignore option value and prematurely invest in flexibility they do not yet need. The famous YAGNI (You Ain’t Gonna Need It) principle is informal option theory: do not exercise the option to build complex infrastructure until the value of that option exceeds its cost.

The important caveat is that options have expiry dates. An option that you never exercise because conditions to exercise it never arrive is simply waste. The team that ships the pragmatic implementation and then never revisits it — because the product succeeds and shipping pressure never relents — has allowed an option to expire worthlessly. They have also accumulated genuine compounding debt. Recognizing this distinction is what separates strategic use of debt from inadvertent accumulation.

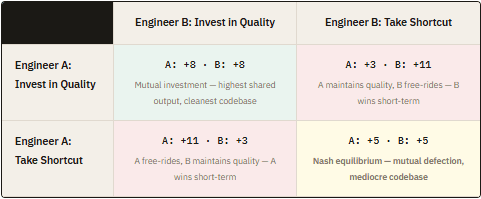

5. The Prisoner’s Dilemma Inside Every Engineering Team

Beyond individual decisions, technical debt is also a collective action problem with a clear game-theoretic structure. The situation inside most engineering teams maps almost exactly onto the classic Prisoner’s Dilemma: each individual engineer has an incentive to cut corners, even though the collective outcome when everyone cuts corners is worse for every individual than if everyone had cooperated on quality.

The payoff matrix works like this. Consider two engineers working on adjacent parts of the codebase. Each can either invest in clean, documented, well-tested code — or ship faster with technical shortcuts.

The Nash equilibrium — the point at which neither engineer has an incentive to unilaterally change their behavior given the other’s choice — is mutual shortcut-taking. Both get a mediocre outcome (+5, +5) when they could have had a good one (+8, +8). This is rational individual behavior producing a collectively irrational outcome.

Several real-world conditions push teams toward the defection equilibrium. Individual performance metrics that reward shipped features rather than code quality. Sprint cycles that create deadline pressure every two weeks. Frequent team turnover that reduces the cost of leaving debt for someone else. Lack of visibility into cumulative debt load. And perhaps most perniciously, the asymmetry of credit: the person who ships the shortcut gets the feature credit, while the person who later pays the interest cost is just “doing maintenance.”

Technical debt is a variant of the “Tragedy of the Commons” — the phenomenon where shared resources are over-exploited by individually rational actors. Each developer who adds debt to a shared codebase imposes a cost distributed across the entire team, while capturing the full benefit of the shortcut personally. Without institutional mechanisms to internalize those distributed costs, over-accumulation is the predictable equilibrium.

6. When Accumulating Debt Is Genuinely Rational

Given the economic models above, we can now be more precise about when choosing to accumulate technical debt is a legitimate, rational business decision — rather than a failure of discipline.

✓ Rational Debt Accumulation

- High organizational discount rate: survival depends on near-term milestones (funding round, market window, regulatory deadline)

- High requirement uncertainty: the feature may be redesigned or abandoned based on user feedback — option value favors deferral

- Short expected system lifespan: a migration or replacement is planned within 12–24 months

- Deliberate and tracked: the debt is recognized, documented, and owned by someone with authority to repay it

- Interest rate is known and low: the shortcut does not touch high-traffic, high-coupling areas where drag compounds quickly

✗ Irrational Debt Accumulation

- Low organizational discount rate: the system has a 10-year horizon and stable requirements, but teams still optimize for this sprint

- Invisible debt: no one knows the total load, making NPV calculations impossible

- Interest compounds on critical paths: debt is accumulating in the areas of the codebase changed most frequently

- No repayment trigger: debt was taken on without any defined condition that would trigger remediation

- Cultural drift: shortcuts become the default rather than the deliberate exception, destroying code quality norms

Notice that the line between rational and irrational is not primarily about code quality. It is about whether the economic parameters that justify taking on debt — high discount rate, high uncertainty, low interest cost, defined repayment horizon — actually apply to the specific situation. The same shortcut is rational in one context and destructive in another.

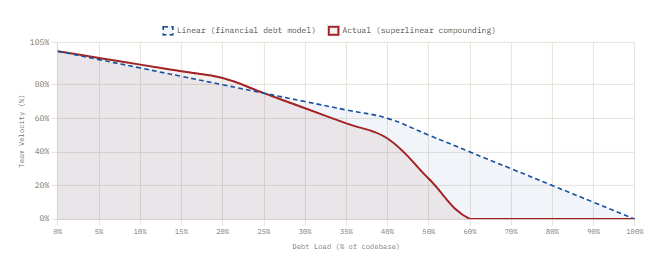

7. The Non-Linear Interest Curve

One of the most important — and most frequently underestimated — economic properties of technical debt is that interest is non-linear. In financial debt, interest accumulates proportionally to principal. In technical debt, it does not. The relationship between debt load and velocity drag is superlinear: small amounts of debt in the right places are manageable; large amounts of debt in high-coupling areas become catastrophic.

This is why the standard financial metaphor, while useful for initial communication, eventually misleads. A business carrying 30% more financial debt than its peers faces a proportionally higher interest burden. An engineering team whose core domain model is entangled with infrastructure concerns does not face a proportionally higher drag — it faces an architectural inflection point beyond which every change requires touching multiple interlocked systems, and the cost per feature grows not linearly but with something closer to O(n²) complexity.

Debt Load vs. Feature Delivery Velocity — The Non-Linear Curve

The empirical data from McKinsey’s 220-company study supports this shape. Companies in the 80th percentile for their Tech Debt Score have revenue growth 20% higher than those in the bottom 20th percentile. Furthermore, companies with the highest debt ratios were significantly more likely to fail or cancel modernization efforts entirely — suggesting that past a certain threshold, debt becomes not just a drag but a trap from which recovery is difficult.

The practical implication is that the discount rate reasoning above — which treats future interest as proportional to present principal — systematically underestimates the true cost of accumulation once the debt-to-codebase ratio exceeds roughly 20–30%. This is the zone where rational decision-making about individual items turns collectively irrational: each addition looks cheap based on current interest rates, but the rate itself is increasing as the foundation degrades.

8. Managing Debt as a Portfolio

If technical debt behaves like financial debt — with principal, interest, non-linear compounding, and risk — then managing it like a portfolio rather than a list of individual items makes far more economic sense. Financial portfolio theory has three relevant lessons for debt management.

1. Differentiate by interest rate, not by age

Not all debt compounds equally. Debt in a module that changes every week has a much higher effective interest rate than debt in stable code that has not been touched in two years. Prioritize repayment by interest rate, not by when debt was incurred. The oldest code is often the most stable — and therefore the least urgent.

2. Set a debt ceiling, not a debt target of zero

One large insurance company described by McKinsey committed to making tech debt a strategic priority at the board level — not to eliminate it, but to manage it within bounds. They established a pricing mechanism on internal IT service costs to fund ongoing debt management. Zero debt is neither achievable nor desirable; the goal is sustainable leverage, exactly as in corporate finance.

3. Repayment should be systematic, not heroic

The engineering equivalent of “we’ll fix this in the next big refactoring sprint” is like planning to pay down a mortgage in one lump sum someday. It rarely happens, and the longer the delay, the worse the terms become. Instead, many successful teams allocate a fixed percentage — typically 15–20% — of each sprint to debt repayment, treating it as an operating cost rather than a capital project.

4. Make debt visible on the balance sheet

Technical debt that is invisible to decision-makers cannot be managed rationally. Teams that have succeeded in shifting the conversation use concrete proxies: change failure rate by module, mean time to add a feature in a given subsystem, test coverage as a proxy for future maintenance cost. These metrics give product managers and business stakeholders the data they need to weigh debt repayment against feature investment on equal economic footing.

| Debt Type | Interest Rate Profile | Repayment Priority | Analogy |

|---|---|---|---|

| Core domain model shortcuts | Very High — touched on every feature | Immediate | High-interest revolving credit card |

| Missing tests on critical paths | High — slows every change, hides bugs | Near-term | Uninsured business risk |

| Outdated dependencies | Medium — security risk grows over time | Planned | Variable-rate mortgage |

| Legacy integration adapters | Low–Medium — high cost but infrequent | Opportunistic | Long-term corporate bond |

| Code style and naming debt | Low — slows onboarding, not delivery | Background | Minor consumer debt |

9. When “Rational” Accumulation Becomes a Trap

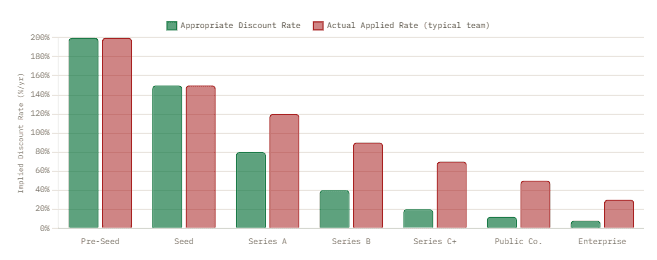

The economic case for accepting debt is real, but it has a known failure mode: the conditions that justified taking on debt change, and the debt does not get repaid. This is not a hypothetical risk — it is the standard trajectory. Most technical debt that becomes genuinely unmanageable began as rational, deliberate decisions that were never revisited.

The mechanism is predictable. A startup takes on debt to hit a Series A milestone. Reasonable. The Series A succeeds, and suddenly there is a team of twenty engineers on a codebase built for five. The discount rate has dropped dramatically — the company now has a much longer time horizon. But the sprint pressure is, if anything, higher because growth objectives demand constant feature velocity. The organizational conditions for repaying debt never quite arrive. Each quarter, the NPV calculation is run implicitly and the result is always “not yet.”

The critical failure mode is not accumulating debt at a high discount rate — that can be rational. It is continuing to apply a high discount rate after the organization’s actual time horizon has lengthened. A startup’s discount rate might reasonably be 150% per year. The same company at Series C should be applying something closer to 15%. Teams that never update their discount rate continue to behave like they are months from running out of money even when they have years of runway.

The game-theoretic dimension compounds this. Even when individual engineers and team leads understand that the discount rate should have dropped, the incentive structures often have not been updated to match. Performance reviews still reward shipping. Refactoring work is still invisible in sprint velocity metrics. The Prisoner’s Dilemma payoffs have not changed even though the optimal strategy has. The result is a team that knows it should be investing in quality but cannot find a way to make that individually rational given the incentives in place.

This is precisely why the CIO observation from McKinsey is so striking: “By reinventing our debt management, we went from 75% of engineer time paying the tech debt ‘tax’ to 25%. It allowed us to be who we are today.” The company in question did not achieve this by telling engineers to write better code. They achieved it by changing the institutional structures — the incentives, visibility, and authority — that had been producing the Nash equilibrium of mutual defection.

When to Repay: Implied Discount Rate vs. Organizational Stage

10. What We Have Learned

Technical debt is not a moral failing. It is an economic instrument with well-defined properties — principal, interest, compounding, and option value — and like all economic instruments, it can be used well or badly. The argument that teams should “just refactor” is economically equivalent to arguing that businesses should “just pay off all their debt.” It ignores the cost of capital, the value of flexibility, and the real trade-offs that operate in every organization running at velocity.

The temporal discounting framework shows why debt is rational at high discount rates — and why updating those rates as organizations mature is critical. The option value model shows why deferring architectural investment is sometimes genuinely optimal, not lazy. The Prisoner’s Dilemma shows that even individually rational engineers can produce collectively irrational codebases without the right institutional mechanisms — specifically, aligned incentives, visible metrics, and systematic (not heroic) repayment. The non-linear interest curve is the piece most commonly missing from the conversation: debt compounds superlinearly past a threshold, which means the individual decision that looks rational when viewed in isolation contributes to a system-level tipping point.

The portfolio model is the practical synthesis: treat different types of debt according to their effective interest rates, set a sustainable debt ceiling rather than aspiring to zero, and build repayment into the operating rhythm rather than waiting for the refactoring sprint that never comes. Most importantly, make the debt visible — not as a confession of past sins, but as a balance sheet item that both engineering and business leadership can reason about together, in the same economic language.