6 min read: Understanding the business logic behind seemingly irrational engineering decisions

Every developer has heard it: “We need to refactor this code.” Every product manager has pushed back: “Can’t we ship first and clean up later?” This tension isn’t a failure of communication—it’s a fundamental economic trade-off that mirrors decisions made across industries, from manufacturing to finance.

The term “technical debt” was coined by Ward Cunningham in 1992, but we’ve been treating it as a moral failing rather than what it actually is: a financial instrument. When we apply proper economic models to technical debt, something surprising emerges—many teams are making perfectly rational decisions to accumulate it.

1. The Time Value of Code

In finance, a dollar today is worth more than a dollar tomorrow. This principle, called the time value of money, drives every investment decision. The same logic applies to software features.

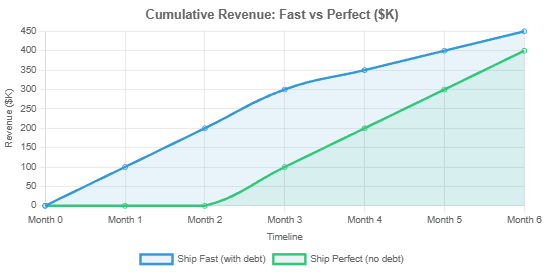

Imagine two scenarios: Ship a feature today with messy code, or ship it in three months with pristine architecture. If that feature generates $100,000 in monthly revenue, the “messy code” option produces $300,000 more revenue over those three months. Even if you eventually spend $50,000 in developer time fixing the mess, you’re still ahead by $250,000.

1.1 The Discount Rate Problem

Companies apply a discount rate to future benefits—typically 10-20% annually for tech companies. This means benefits next year are worth only 80-90% of benefits today. When engineering teams argue for refactoring that will save time “eventually,” they’re fighting against this mathematical reality.

Here’s the uncomfortable truth: A startup with 18 months of runway should have a much higher discount rate than Microsoft. The startup might rationally discount future benefits at 50% or more, because there’s a real chance they won’t exist to reap those benefits. This isn’t short-term thinking—it’s survival.

| Company Stage | Typical Discount Rate | Rational Tech Debt Strategy |

|---|---|---|

| Pre-product-market fit startup | 40-60% | Accumulate aggressively; optimize for learning speed |

| Growth-stage startup | 20-35% | Selective accumulation; pay down blockers |

| Mature company | 10-15% | Maintain low levels; invest in platform quality |

| Declining market share | 30-50% | Strategic accumulation to fund pivots |

2. Option Value and Strategic Flexibility

Technical debt creates something economists call option value. By deferring architectural decisions, you preserve the ability to make better choices when you have more information.

Consider a team building a payment system. They could architect it today to handle international currencies, multiple payment processors, and cryptocurrency. Or they could build a simple system that works for their current US market. The second approach accumulates technical debt—but it also preserves options.

Key Insight: If there’s a 30% chance you’ll pivot away from payments entirely, over-engineering the payment system destroys value. You’ve paid the full cost of a feature you’ll abandon. Technical debt in this context is actually risk management.

2.1 The Real Options Framework

Game theory gives us a framework called real options, typically used for investment decisions. Applied to technical debt:

Call Option: Technical debt gives you the option to invest more later. You keep the codebase simple now, preserving the option to build complexity when (and if) it’s needed.

Put Option: Clean architecture gives you the option to abandon features easily. Well-isolated code can be deleted without cascading effects.

The question isn’t “should we have technical debt?” It’s “which option is more valuable given our uncertainty?”

3. The Compound Interest Problem

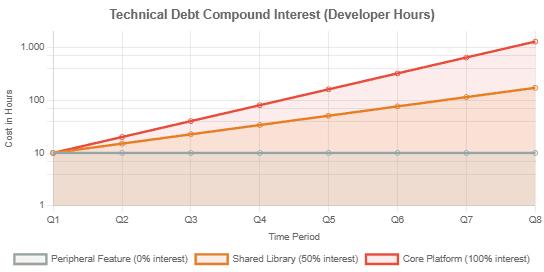

Where technical debt differs from financial debt is in its interest rate. Financial debt compounds predictably—5% annual interest is 5% forever. Technical debt compounds unpredictably and often exponentially.

A quick hack in a rarely-touched module might carry 0% interest—it never gets worse. But a hack in your authentication system might carry 200% interest as every new feature needs to work around it. The challenge is that interest rates are hard to predict upfront.

3.1 When Interest Rates Explode

Research from the Software Engineering Institute identifies scenarios where technical debt interest compounds fastest:

- Platform code – Every application team pays the interest

- Data models – Migrations become exponentially expensive

- Security systems – Debt creates expanding attack surfaces

- Integration points – Complexity grows with each connection

Rational teams pay down debt in these areas quickly, while tolerating it in peripheral features. This explains why “just refactor it” is bad advice—you need to refactor the right things.

4. Game Theory: The Tragedy of the Commons

Technical debt exhibits classic tragedy of the commons dynamics. Each team makes locally optimal decisions that are globally destructive.

Team A needs a feature fast. Taking on technical debt benefits Team A immediately (fast shipping) while distributing costs across all future teams. In game theory terms, this is a negative-sum game—the total value destroyed exceeds the value created.

| Scenario | Team A Benefit | Company Cost | Net Value |

|---|---|---|---|

| Quick hack in shared library | +$20,000 (faster shipping) | -$60,000 (6 teams affected) | -$40,000 |

| Messy code in isolated service | +$20,000 (faster shipping) | -$15,000 (only Team A affected) | +$5,000 |

| Proper solution upfront | $0 (delayed shipping) | -$30,000 (extra development) | -$30,000 |

This explains why governance matters. Without proper incentive structures, rational actors will over-accumulate technical debt even when it’s company-destructive.

5. Legitimate Business Trade-Offs

When someone says “just refactor it,” they’re ignoring several legitimate constraints:

5.1 Information Asymmetry

Developers see the technical cost. Product managers see the opportunity cost. Neither has complete information, creating what economists call information asymmetry. The developer doesn’t know that the competitor is about to launch the same feature. The PM doesn’t know that the “quick fix” will block three future projects.

5.2 Risk Profiles

Companies with different risk profiles should make different technical debt decisions. A regulated healthcare company should carry less technical debt in compliance systems than a social media startup should carry in recommendation algorithms. This isn’t one side being “more responsible”—it’s different risk-adjusted returns.

5.3 Market Timing

Sometimes being first to market with a messy solution beats being second with a perfect one. Instagram famously had massive technical debt in its early days, but the network effects from rapid user growth made the debt manageable. Had they spent six more months architecting perfectly, they might have been replaced by a fast follower.

Strategic Consideration: Technical debt should be evaluated against competitive dynamics, not just internal engineering preferences. A technically imperfect product that captures a market can always be refactored. A perfect product that launches too late cannot.

6. Optimal Debt Management

The goal isn’t zero technical debt—it’s optimal technical debt. Just as companies maintain optimal debt-to-equity ratios, engineering teams should maintain optimal tech-debt-to-codebase ratios.

6.1 Leading Indicators

Smart teams track leading indicators of excessive technical debt:

- Cycle time increasing for similar features

- Bug rates rising in older code

- Developer satisfaction declining

- Deployment frequency decreasing

These metrics signal when technical debt interest is compounding dangerously. Many teams from companies like Spotify and Amazon publish their approaches to measuring and managing this balance.

6.2 Strategic Repayment

Optimal repayment follows economic principles:

- Pay high-interest debt first – Refactor what’s blocking multiple teams

- Refinance when rates drop – When market pressure eases, invest in foundations

- Default strategically – Sometimes it’s cheaper to rewrite than refactor

7. What We’ve Learned

Technical debt isn’t a failure of discipline—it’s a financial instrument that can be wielded strategically or destructively. Teams that treat it as a moral failing miss opportunities to make rational trade-offs. Teams that ignore its compounding interest destroy long-term value.

The mathematics are clear: Early-stage companies should rationally carry more technical debt than mature ones. Features with uncertain futures should be built with more debt than core platform code. And “just refactor it” ignores the time value of shipping, option value of flexibility, and legitimate business constraints.

The best teams don’t eliminate technical debt—they manage it like any other business resource, with clear metrics, honest trade-off discussions, and strategic investment in the areas where debt is most expensive. When developers and business stakeholders understand these economic principles, they can move from frustrating arguments to productive negotiations about how much debt is optimal given their specific constraints.

The next time someone proposes taking on technical debt, ask about the discount rate, the option value, and where the interest will compound. And when someone says “just refactor it,” ask what opportunity cost they’re willing to pay. These aren’t engineering questions or business questions—they’re economic questions, and they deserve economic answers.